But this does not always play out as expected. At times, the subsidiaries never come into their own. With persistent losses, they can bleed out the parent company’s financial might. In such cases, the standalone financials may look healthy or even impressive. But a look at the consolidated financials paints a sad picture.

In this article, we shall examine three cases in which struggling subsidiaries have been deadweights for their parents.

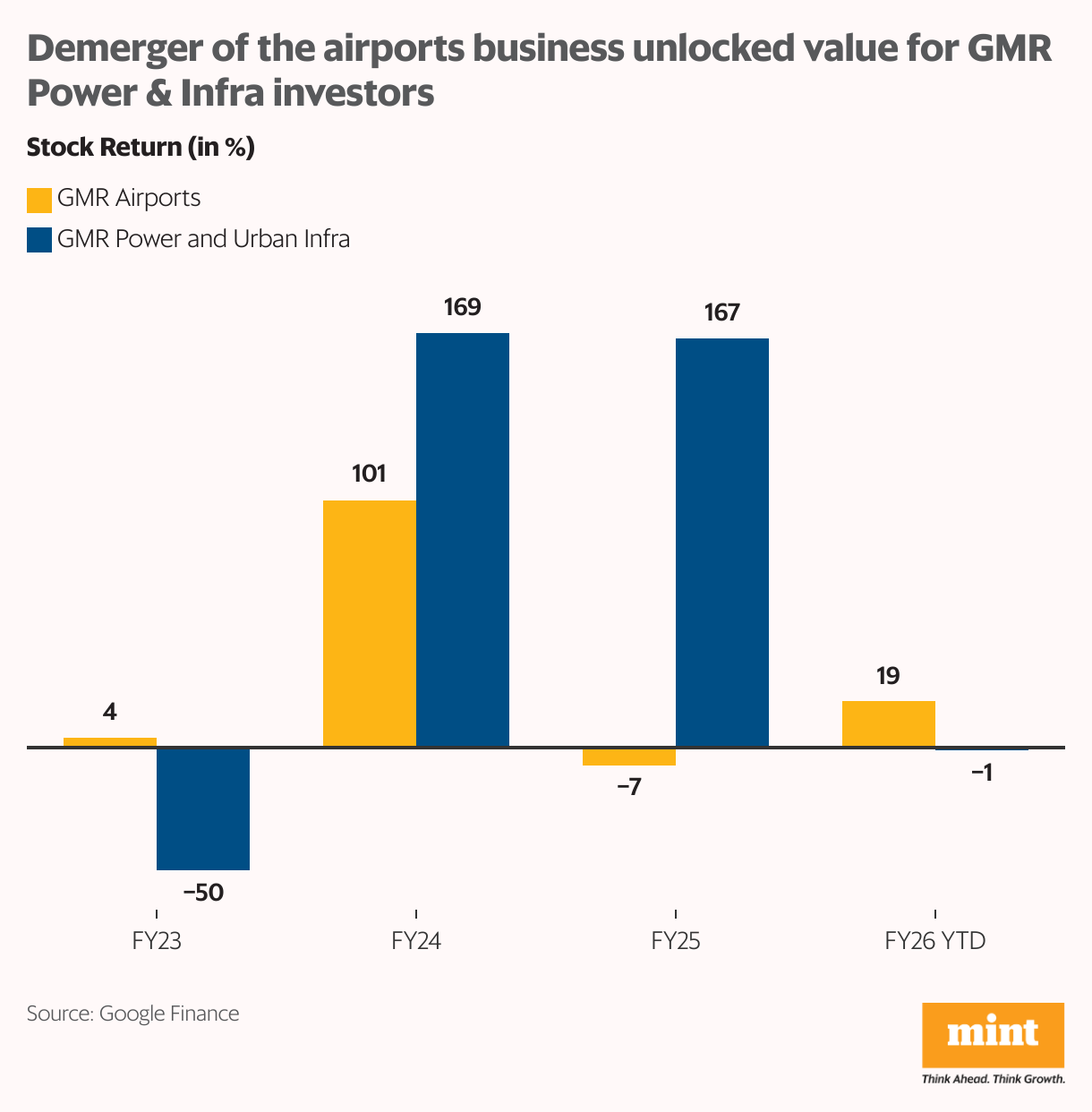

GMR Infra – Demerger unlocked investor value

The GMR group is engaged in a wide range of businesses from airports and energy to transportation and urban infrastructure. But problems had plagued the group across companies. While its power business struggled under low utilizations leading to low operating leverage and shrunk margins, regulatory uncertainty affected the financial viability of some of its airports. The overall group was faced with delayed projects and mounting debt, leading to interest costs which ate away at profitability.

To solve this, the group divested non-core assets, raised funds, and pared down debt. As part of the process, it had to bring in strategic investors. Since such investors tend to look for pureplay businesses, the GMR group was demerged—its airport projects were split up into a separate company, GMR Airports Ltd, while the remaining businesses were renamed GMR Power and Urban Infra Ltd.

This “de-consolidation” of unrelated businesses allowed pulling in a strategic investor for its airports business–France-based Aéroports de Paris (Groupe ADP). It also enabled the management to streamline focus on the businesses and unlocked investor value.

In FY25, GMR Airports reported more than Rs10,000 crore in revenues, but continued to pile on losses. On the other hand, GMR Power and Infra Ltd. reported ₹1,400 crore in profits on a topline of about ₹6,000 crore. GMR Power and Infra Ltd has almost quadrupled investor wealth since FY23 with a CAGR of 47%, while GMR Airport has lagged behind with a CAGR of less than 30% during the period.

Andhra Sugars – Jocil drags down profitability

Established in 1974, Andhra Sugars had started as a sugar manufacturer. Over the years, it has diversified into multiple businesses, including chlor-alkali products, industrial chemicals, soaps, and power generation. Sugar now contributes just about 6% to the company’s revenues, with 40% coming from industrial chemicals, and 33% from chlor-alkali products.

Despite a diversified business profile and a healthy balance sheet, the company has been posting quarter after quarter of underwhelming results. Weak demand and lower realisations have resulted in underutilization of capacity and unfavourable operating leverage, putting the company’s margins under pressure.

Matters have been made worse by its subsidiary, Jocil Ltd. Jocil manufactures fatty acids, stearic acid, refined glycerin, soap noodles, and toilet soap among other similar products. It is also engaged in manufacturing industrial oxygen, and biomass and wind-based power-generation. In FY25, the subsidiary contributed ₹870 crore in operating income towards Andhra Sugars’ consolidated revenue of ₹2,020 crore.

But Jocil’s margin profile leaves nothing on the table for investors. With 50% of its revenues coming from a single customer, the company has almost no pricing power. Coupled with rising raw-material prices, which could not be passed through to customers amid intense competition, its net profit margin stood at a paltry 0.12% in FY25. Over the near term, the moderation in crude prices, which constitute more than 80% of soap revenues, is expected to offer some relief.

However, the lack of pricing power at a significantly sized subsidiary that is vulnerable to crude-price fluctuations can continue to intermittently drag down the consolidated margins for Andhra Sugars.

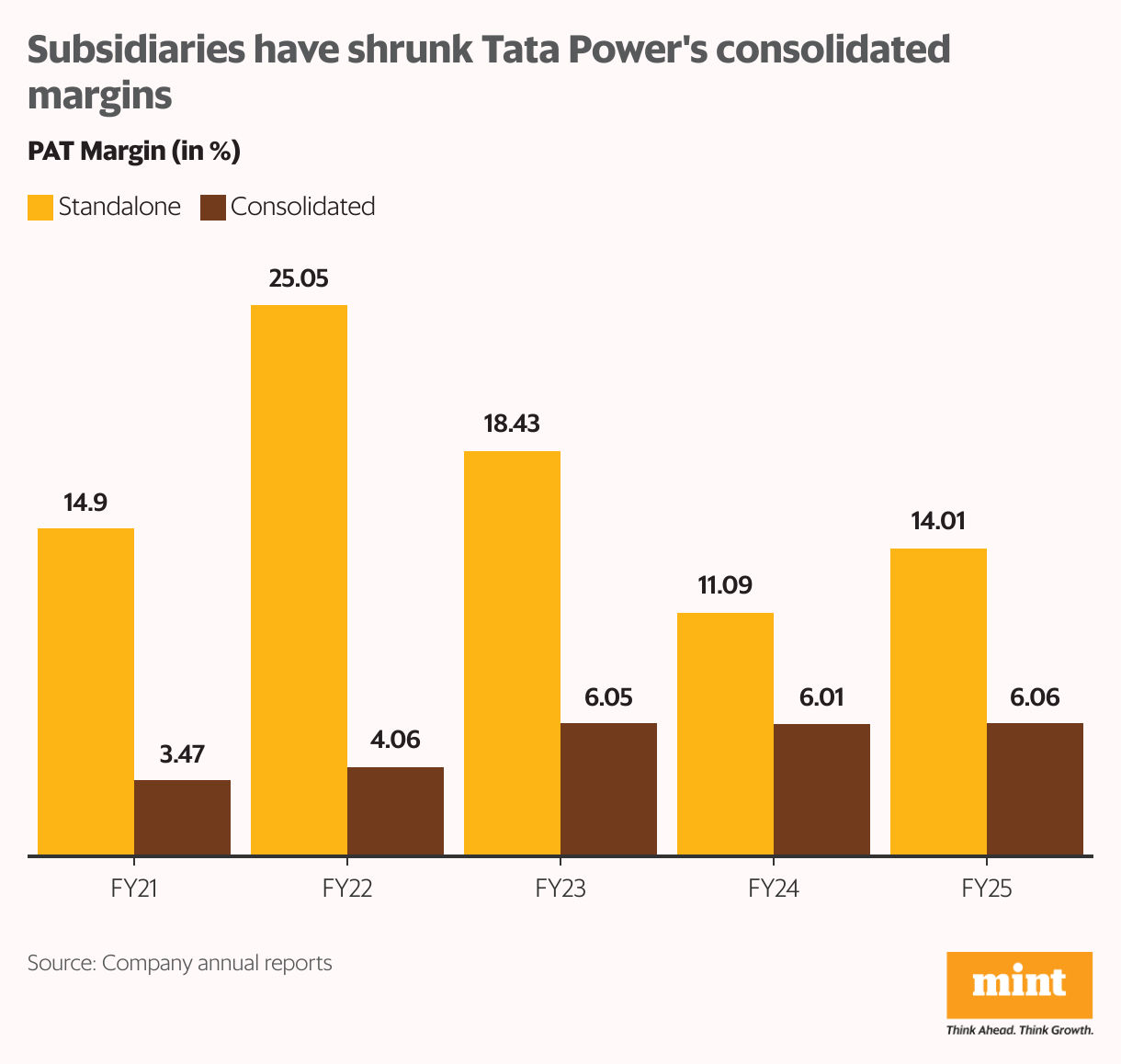

Tata Power – The Mundra matter, and more

Tata Power is India’s leading player in power generation, transmission, and distribution. It is also investing towards expanding renewable energy capacity. Long-term power-purchase agreements (PPAs) drive most of its power production, ensuring extended revenue-visibility. It is backward integrated as well, with long-term fuel supply agreements in place with domestic and international coal miners.

Of course, complications arise in the management of receivables from state discoms. But the issue has been kept under control with the implementation of late-payment surcharge rules. The standalone business’ operating efficiencies and cash-flow management are robust. The problem posed by its subsidiaries, however, is an entirely different ball game.

The company’s Mundra power plant has been a drag since its commencement in March 2013 under Coastal Gujarat Power Ltd (CGPL). Problems started due to changes in Indonesia’s mining regulations which pushed up the cost of coal imported by CGPL. This had made existing PPAs signed by CGPL unviable. Result? Consolidated margins have been significantly impacted over the years.

In 2023, under section 11 of the Electricity Act, Tata Power was allowed to pass through the higher costs of coal (after adjusting the profits made by its coal-mining business). This, along with moderating coal prices, have helped improve the financials of CGPL. Losses have reduced, but profitability is still some way away. And so is a sustainable long-term solution.

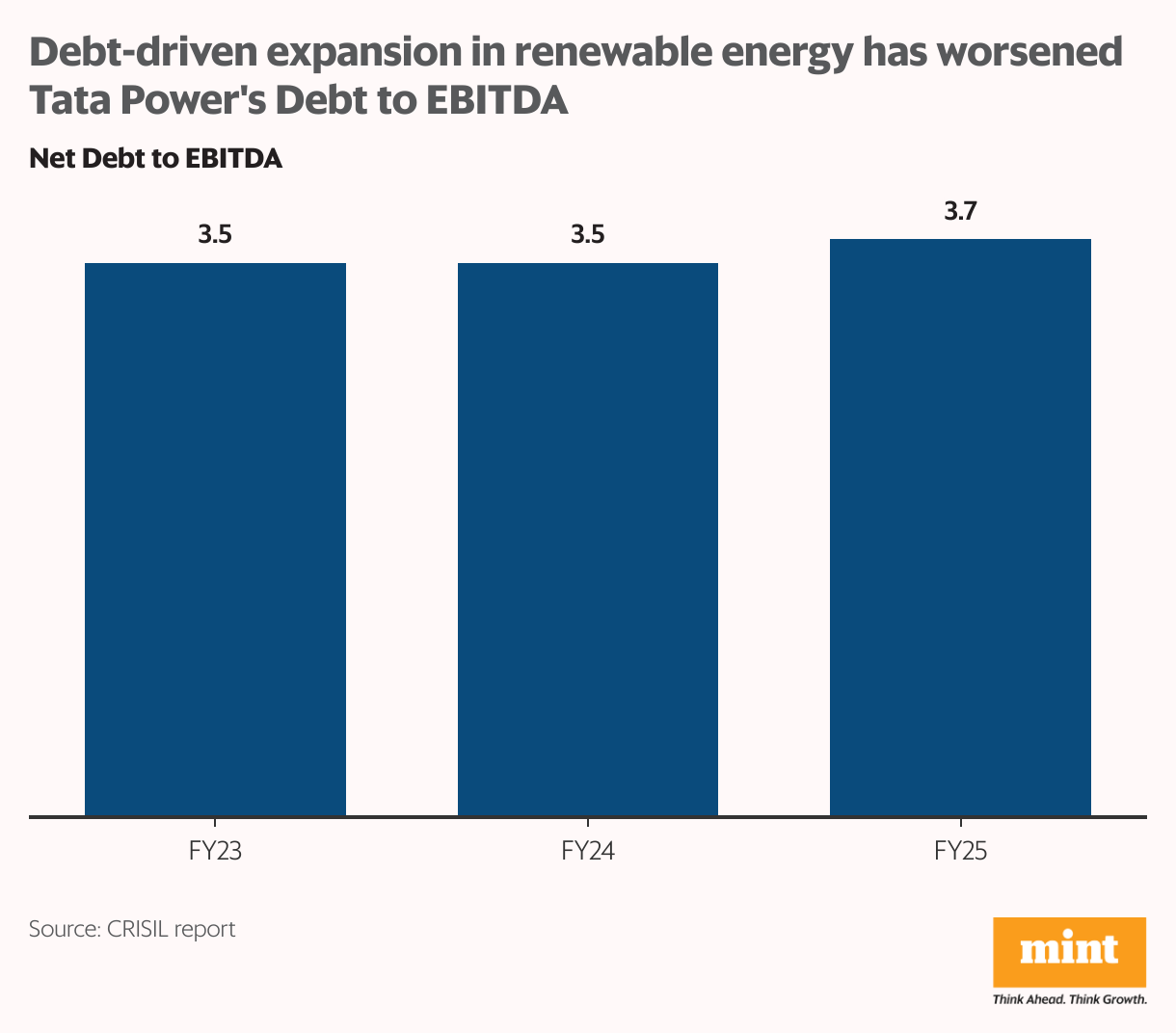

And now, another subsidiary is making investors anxious – Tata Power Renewable Energy Ltd. Debt-funded renewable capacity expansion from 4.5 GW to 5.5 GW has worsened Tata Power’s debt to Ebitda from 3.5 in FY24 to 3.65 in FY25. Of course, debt coverage has improved on the back of improving profitability. But another 5.4 GW of renewable capacity is under development, and the company plans to add roughly ₹20,000 of debt this fiscal. Execution challenges and price fluctuations could also further stress Tata Power’s consolidated financials.

For more such analyses, read Profit Pulse

Rounding it up

It won’t be fair to expect a subsidiary to start contributing positively from day one. Initially, it may post losses and require direct or indirect financial support from its parent. But if a subsidiary persistently drags down the consolidated performance, it is better to cut losses and lose the dead weight. In fact, it may so happen that the dissociation is crucial for even the subsidiary’s survival. This is what we saw in the case of GMR Infra, where the demerger of its airports business was pivotal to pull in a strategic partner.

This may be easier said than done, however. A parent and its subsidiaries are often linked in ways which go beyond shareholding. For example, Jocil Ltd. has been receiving investment-grade credit-ratings, thanks primarily to Andhra Sugars’ backing. And with CGPL, had it not been for Tata Power’s financial support, persistent losses would have taken down the Mundra plant years back.

That said, subsidiaries can cut the other way around as well. Consider for instance, companies like Essar Port where the parent’s revenues and profits are barely a fraction of the consolidated financials. This is to say that subsidiaries are not red flags by rule. But when it comes to diversified conglomerates, it is important to consider the consolidated financials and apply the appropriate holding company discount before making investment decisions.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser.

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.