A weaker-than-anticipated June quarter (Q1FY26) result of Tata Consultancy Services (TCS) Ltd has raised concerns about a further delay in revenue revival. It has got investors wondering about whether or not the earnings downgrade cycle for the sector has bottomed out or if there is more pain ahead. Sequential constant-currency (CC) revenue fell 3.3% versus the Bloomberg consensus estimate of a 1.4% decline in Q1 FY26. The miss was largely driven by the ramp-down of the BSNL project and a sequential CC revenue drop in international markets.

Clients remain cautious, with cost optimization, vendor consolidation and efficiency-led technology transformation as priorities, the management said. Discretionary IT spending remains under pressure. However, demand for GenAI, cloud adoption and platform modernization was firm. Banking and financial services saw pockets of softness, especially in US insurance. Consumer-facing sectors, particularly retail and automotive, were adversely impacted by project deferrals and funding delays due to macro headwinds and delayed decision-making cycles in key markets like North America.

Despite a disappointing start, the TCS management is confident of achieving better revenue growth in FY26 versus FY25 for international business. But the Street is hardly convinced, prompting a cut in earnings per share estimates by various brokerages. The TCS stock fell 3.5% on Friday. “With developed markets now in decline, sequential growth flattish for the last 11 quarters and broad-based decline across verticals, it appears demand issues are deeper,” said an Ambit Capital report of 11 July. The implied ask rate for the international business in Q2-Q4 is 1.1% and given weaker H2 FY26 seasonality and Q2 commentary, any material beat might be tough, Ambit cautioned.

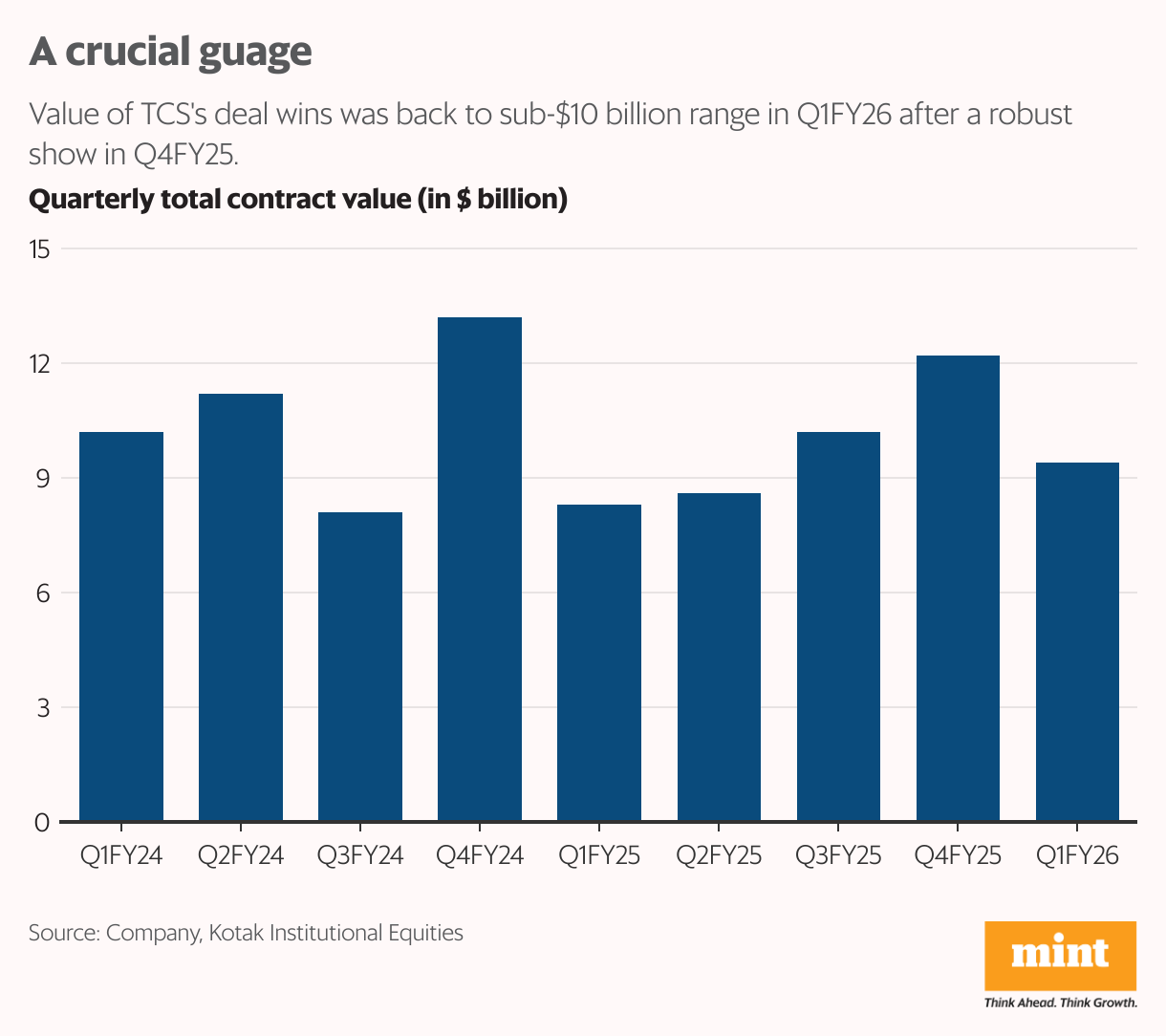

TCS bagged deals with a total contract value of $9.4 billion, up 13.2% year-on-year, aided primarily by cost optimization projects. But the problem of strong deals not translating into growth, implying weak revenue conversion, persisted in Q1 FY26 as well. While this issue is not unique to TCS, it is troubling for sure. “Decline of $50 million+ clients by 9 (6% of the base) in the past four quarters– the highest ever–suggests the challenge is secular. Client-specific decline, such as at Deutsche Bank, might be impacting it too. Understandably, investors worry that TCS is losing wallet share to competition,” said a 10 July JM Financial Institutional Securities Ltd report.

Moreover, the pace of execution is lagging. “While TCS attributed the weak performance in the international business to macro-related uncertainty, we believe execution could have been better,” said the Kotak Institutional Equities report of 10 July. Kotak has identified a few symptoms (of execution slippages) such as weak performance across many verticals and geographies, continued underperformance in the healthcare vertical, lack of mega deals in the past few years, excluding BSNL and JLR (Tata Group entity) and sharp revenue contraction in the top account in TCS E-Serve subsidiary.

Earnings before interest and tax (Ebit) margin expanded 30 basis points sequentially to 24.5%, primarily led by lower costs pertaining to the BSNL deal. TCS would continue to focus on structural levers of utilization improvement, pyramid optimization, and productivity enhancement to save margin. Note that TCS has yet to decide on wage hikes for FY26.

Meanwhile, the TCS stock has recovered from its 52-week low of ₹3,056.05 seen on 7 April following the Liberation Day tariffs announcement. But the lack of macro tailwinds makes meaningful stock revival or earnings upgrades elusive for now. TCS is trading at an unappealing FY27 price-to-earnings multiple of 22x, showed Bloomberg data. According to Ambit, Q1 results confirm a much weaker FY26 for TCS, and Q1 decline implies a steep 2.5% compound quarterly growth rate over Q2-Q4 for even a flat year.