IndusInd Bank stock’s reaction to its June quarter results (Q1FY26) was muted. The numbers were bad as anticipated, but look worse if the consolidated net profit of ₹604 crore, which declined 72% year-on-year, is adjusted for volatile trading gains of ₹469 crore (post average tax rate of 25%).

This was the first clean quarter after Q4FY25, which saw a clean-up of past accounting irregularities. Thus, a comparison of financials, either year-on-year or sequentially, is distorted due to one-offs and reclassification of incomes under various heads. Nevertheless, Q1FY26 performance suggests IndusInd’s outlook appears bleak for FY26 even after factoring in the seasonally stronger second half of the year for the banking sector.

The key event awaited now is the appointment of a regular chief executive officer (CEO) at the helm, as the bank is currently being managed by a committee of executives. The committee refrained from giving any guidance in the Q1 earnings call. If a seasoned lending professional joins in as CEO, investors of the bank can heave a sigh of relief, as there would be clarity on a strategic roadmap.

IndusInd’s balance sheet size, prima facie, shows 2% year-on-year growth to ₹5.39 trillion as on June, but it may be masking the actual pain as a lot of money was raised from certificate of deposits.

The money was raised as the bank maintained higher-than-normal liquidity to manage potential deposit outflows, fearing panic following the disclosure of accounting irregularities. While additional idle funds worth ₹45,000 crore meant a liquidity coverage ratio of 141%, it puts pressure on net interest margin (NIM).

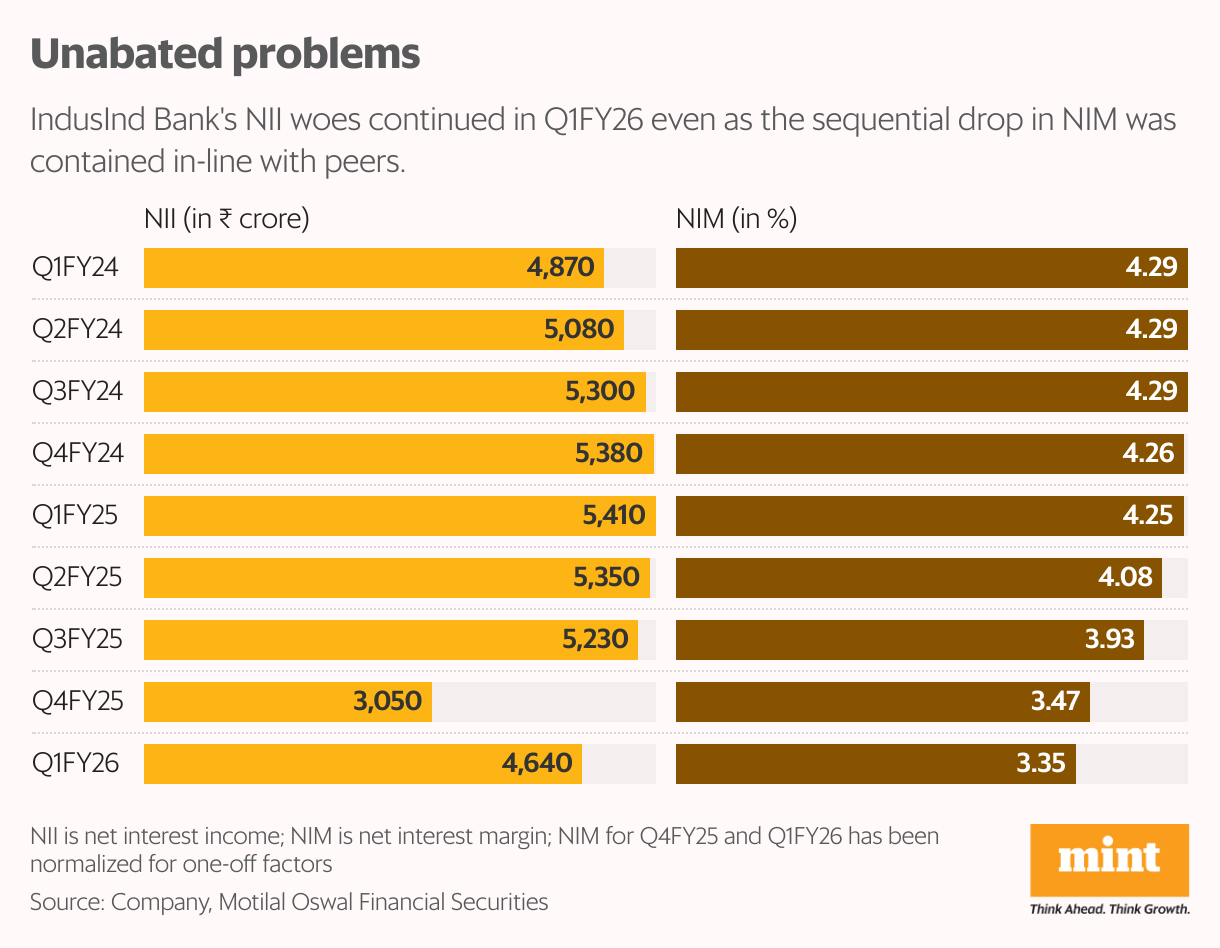

The silver lining is that the drop in IndusInd’s adjusted NIM of 12 bps QoQ was contained and almost in line with the drop seen by HDFC Bank and ICICI Bank.

IndusInd’s Q1FY26 reported NIM was 3.46% and includes an 11 bps benefit due to the recovery of an NPA account and interest on income tax refund. NIM was 2.25% in Q4FY25, while adjusted for earlier accounting discrepancies, it was 3.47%.

Also Read: Sebi retracts words ‘board note’ from IndusInd Bank order, says it was ‘engagement note’

IndusInd’s Q1FY26 core fee income fell 35% year-on-year to ₹1,532 crore led by cards and distribution fees, which declined 55% to ₹296 crore. The management also attributed the fee income drop to the decline in corporate credit book, which has not been too remunerative versus retail credit.

Moreover, the 76% sequential fall in the income looks steep as Q4 tends to have more distribution fees from third-party products such as insurance and mutual funds.

Gross NPA rose 51 bps QoQ to 3.64% of gross advances. The trend was the same for net NPA which rose 17 bps QoQ to 1.12% of net advances. The management stated that its micro finance loans generally see an uptick in NPA from Q4 to Q1 and also pointed out state-level issues regarding the recovery of loans etc.

It is also worth noting that IndusInd has 40% of its loan portfolio in vehicle finance, microfinance, credit cards and personal loans. These segments have been facing tough business conditions at the macro level.

Thus, after a poor Q1, achieving the FY26 Bloomberg consensus net profit estimate of ₹4,108 crore looks like a tall task for IndusInd, raising the risk of downgrades in earnings estimates.

The stock continues to trade below its projected book value of ₹861 for FY26, as per Bloomberg consensus, but the price-to-book value of less than 1x may not be viewed as attractive by investors owing to the single-digit RoAE (return on average equity) of 6%.