With refurbishing centres across India and 38 other markets including the US, the UAE, and countries in Europe and Africa, GNG has a dominant position in the growing market for affordable and sustainable tech.

At the heart of the IPO is a strategic push to pare debt. Of the IPO proceeds, ₹320 crore has been earmarked for repayments. Will this allow the company to bolster its balance sheet and accelerate it expansion plans? And what else should investors know about the reuse revolution it’s driving?

Also read Q1 moves: Retails investors bet big on property, cement and auto parts as ‘smart money’ retreats

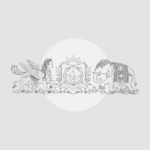

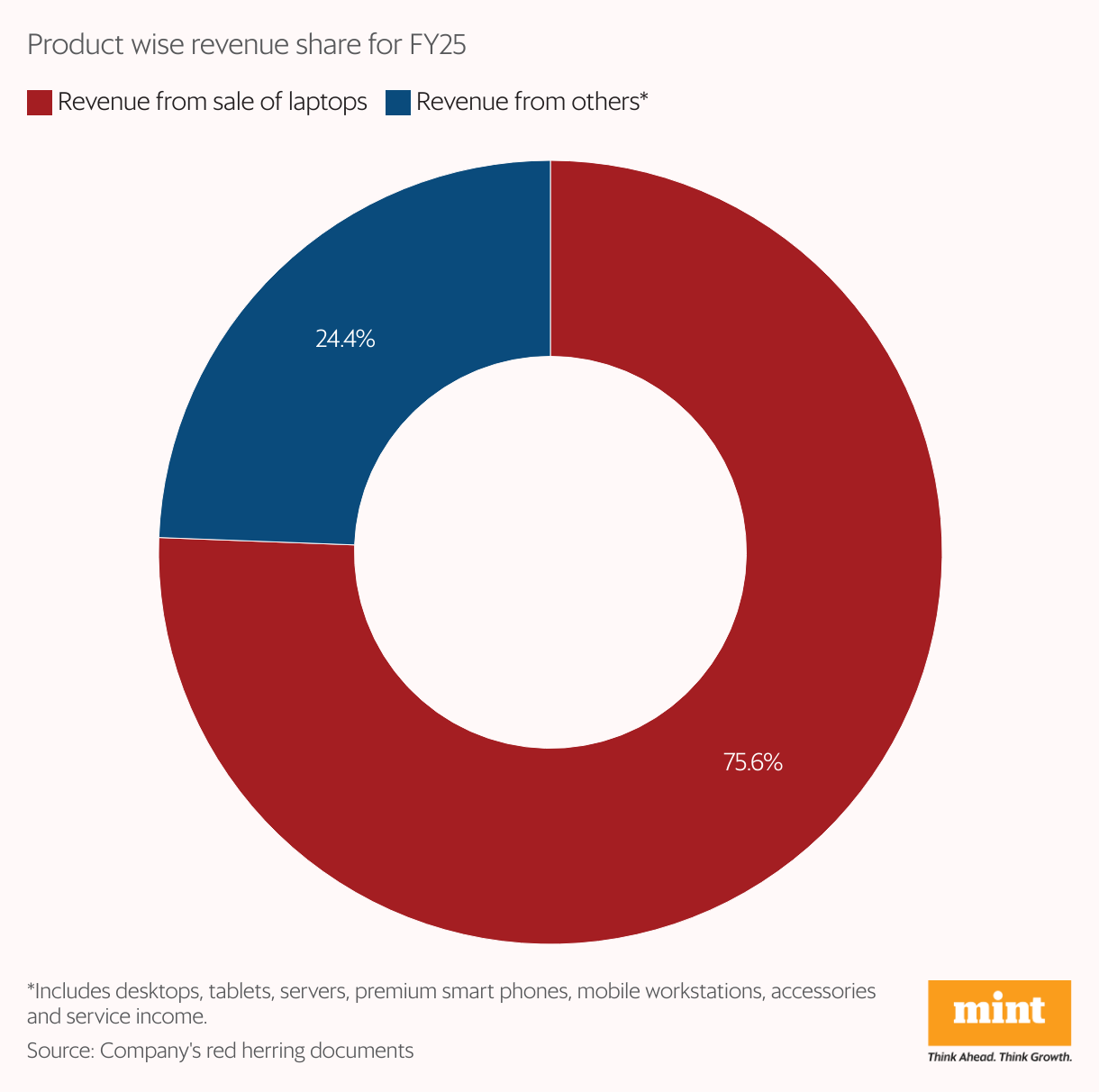

What is the breakdown of GNG’s revenue by product category and markets?

Refurbished laptops were GNG Electronics’ primary revenue driver in FY25, contributing nearly 76% of sales. The remaining 24% came from a diverse portfolio including desktops, tablets, servers, premium smartphones, accessories, and various services.

The Middle East was the dominant market, accounting for about 51% of revenue. India contributed about a quarter of total revenue, while the US contributed about 18%.

Apart from being India’s largest Microsoft-authorised refurbisher, what are GNG’s core, sustainable competitive advantages that differentiate it from both organised and unorganised competitors?

The unorganised sector dominates India’s refurbished PC market, holding an 86.8% share. The organised segment remains highly fragmented, with no single player commanding more than 5%. This dominance of the unorganised market presents significant operational challenges for organised players.

However, GNG stands out. Apart from being India’s largest Microsoft-authorised refurbisher, the company has several key differentiators that give it a competitive edge. First, GNG is a truy global company, with operations spanning the US, Europe, the UAE and other major economies, which provides crucial global supply chain and relationship advantages.

Second, its fully integrated operations—from procurement and refurbishment to sales and after-sales service—create substantial entry barriers for competitors. This comprehensive approach, combined with deep technical expertise in repairing and refurbishing a wide range of electronics gives GNG a unique position in a fragmented industry.

What specific expertise does the management team have?

Beyond general leadership, GNG’s management team brings deep functional expertise across operations, finance, business development, engineering, legal, HR, and international markets.

Founder Sharad Khandelwal has 29 years of experience in information and communication technology. This cross-functional strength helps GNG efficiently scale its refurbishment operations, explore new markets, and maintain consistent product quality with its 949 skilled technicians.

Also read India’s IPO boom cools in 2025. Can the market regain its momentum?

How diversified and robust is GNG’s sourcing network for refurbished devices and their components? To what extent does GNG rely on original equipment manufacturer (OEM) parts versus third-party components?

The company operates a well-diversified global sourcing network, procuring refurbished ICT devices from over 20 countries, including the US, Canada, Germany, the UK, the UAE, Singapore, and Australia. The company uses an independent procurement model and balances cost with quality by sourcing both original OEM parts and high-grade third-party components as needed. This broad supplier base, managed through structured, purchase-order-based agreements, aims to prevent over-reliance on any single vendor.

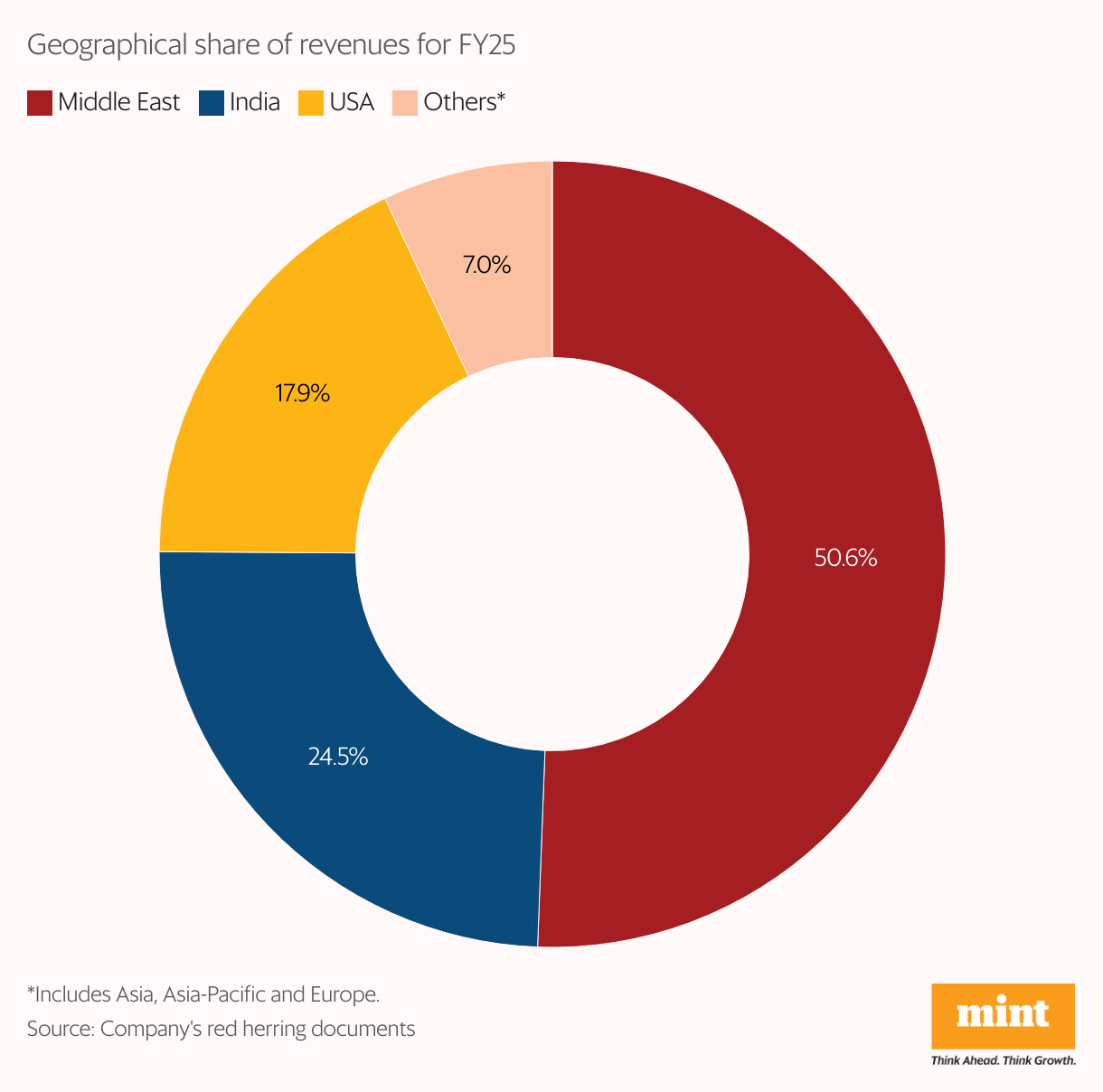

However, GNG faces significant supply-chain concentration risk. Despite its broad network, a substantial 57% of its inventory is sourced from just its top 10 suppliers. This, coupled with an absence of long-term contracts, makes GNG vulnerable. Any price increases or supply disruptions from these critical suppliers could have a disproportionate impact on operations and profitability, exposing the stock to increased volatility.

What is the degree of customer concentration within GNG, specifically outlining the revenue contribution from its top 10 customers?

Over the past three fiscal years (FY23 to FY25), GNG has derived 44% to 56% of its revenue from its top 10 customers, including related-party transactions. This leaves the company vulnerable to expired contract, adverse changes in customers’ financial health, and shifts in demand. While GNG has not experienced material disruption from this concentration in the past three years, there is no guarantee of future business volumes or favourable terms.

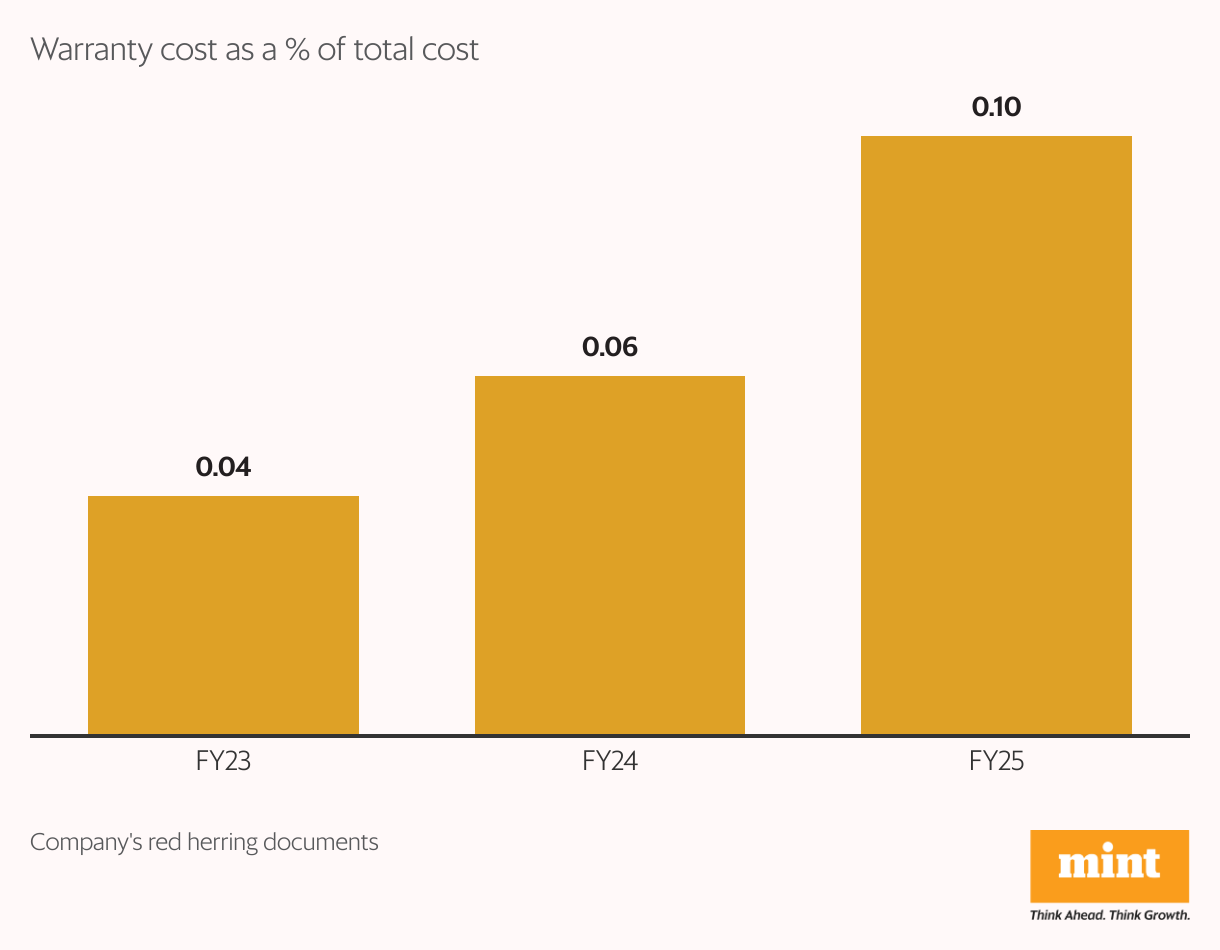

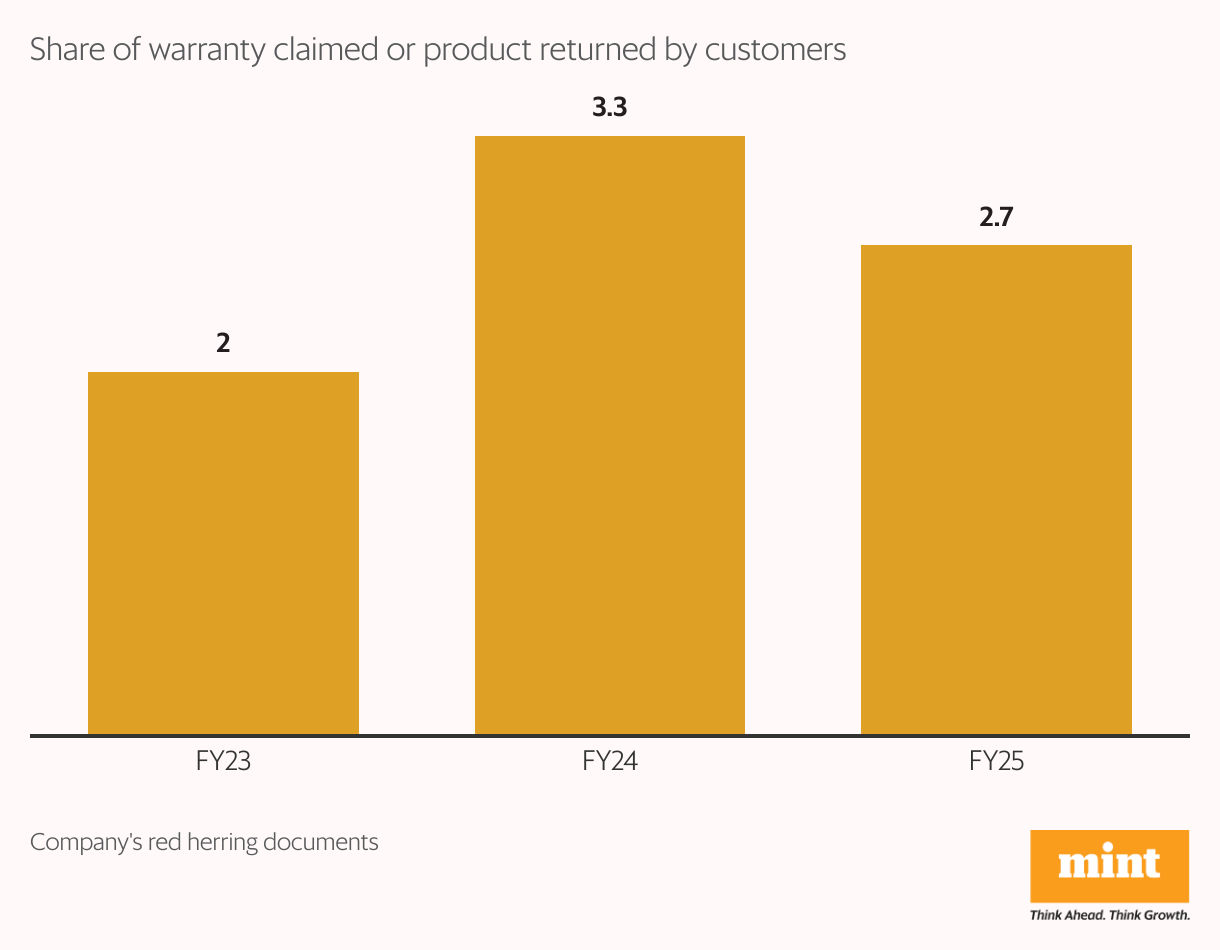

What is the detailed cost structure associated with GNG’s after-sales service and warranty provisions?

GNG offers a one to three-year warranty on its refurbished ICT devices. Warranty costs as a percentage of total costs have risen from 0.04% in FY23 to 0.10% in FY25, correlating with an increase in customer return rates.

The upward trend suggests a challenge in predicting the long-term durability of refurbished devices, given their limited usage history. While no major quality issue has surfaced in recent years, higher claims or product failures could hit margins and expose GNG to liability risks.

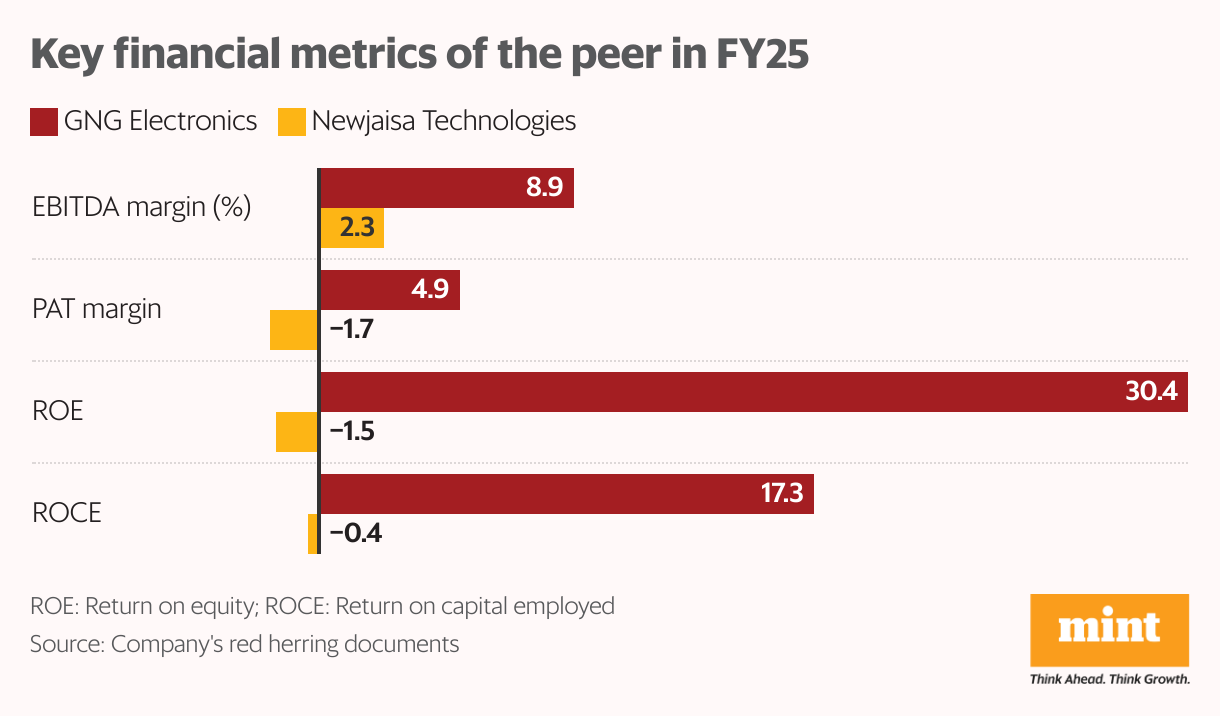

How do GNG’s profitability metrics stack up against those of its peers, and what are its realisations per refurbished unit?

While Newjaisa Technologies, GNG’s listed peer, reported higher margins in FY23 and FY24, it subsequently posted negative profitability metrics in FY25. In contrast, GNG maintained profitability across all key metrics in FY25, demonstrating greater stability and operational resilience.

However, GNG’s realisations per refurbished unit declined from ₹1,307 in FY23 to ₹1,168 in FY25. This warrants close attention, as the company’s ability to stabilise or improve per-unit realisations while sustaining overall profitability will be crucial for its long-term competitiveness and creating value for shareholders.

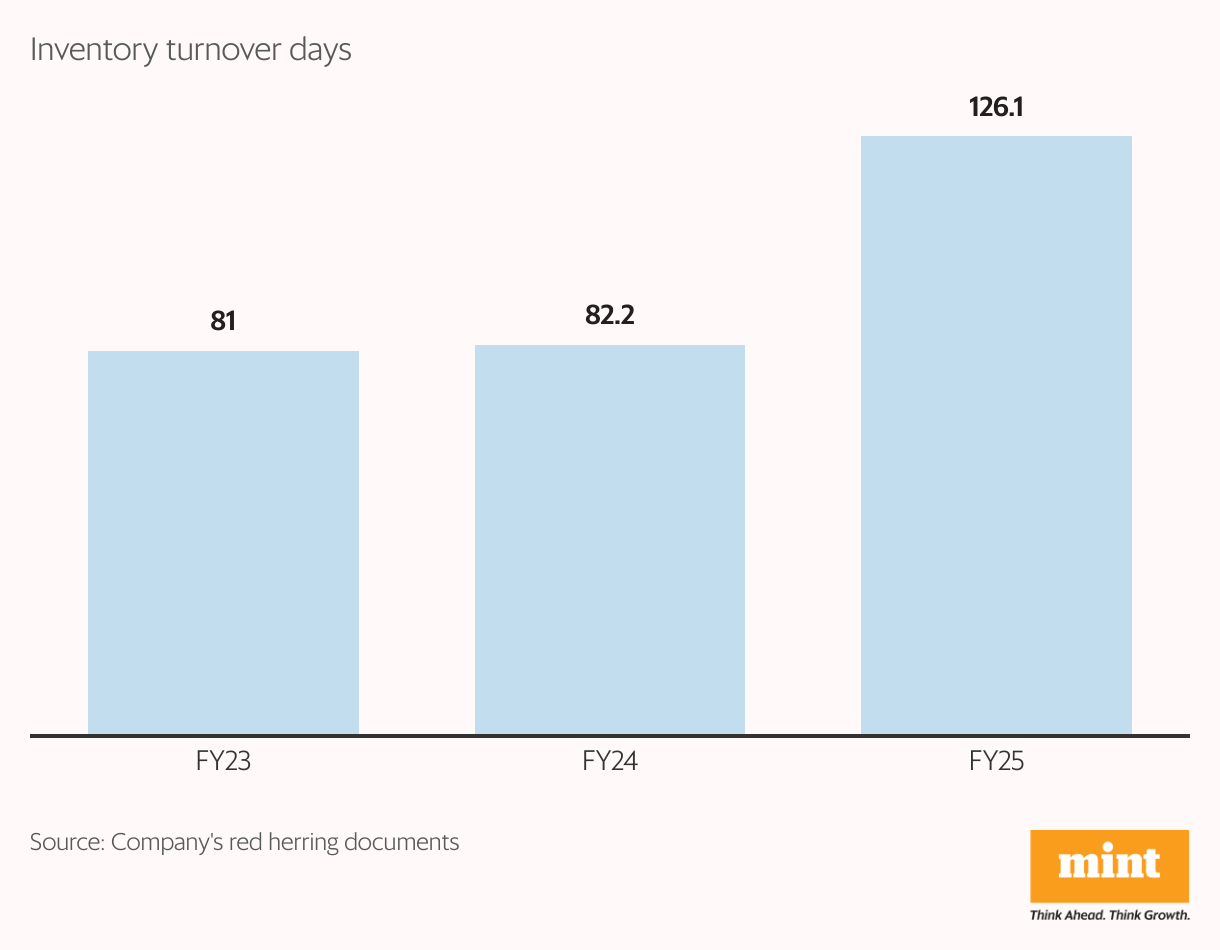

What are the key operational metrics GNG tracks to indicate its efficiency in the refurbishment process and supply chain? Does a rise in inventory turnover days indicate specific operational challenges within GNG?

GNG gauges its operational efficiency through key metrics such as sourcing volume, procurement turnaround, and refurbishment cycle time. Its performance is critically reliant on steady access to used ICT devices, which depends on various factors including corporate upgrade cycles, consumer behavior, and evolving e-waste regulations.

While a diversified supplier base has historically helped maintain supply, rising competition and shifts in market dynamics could lead to higher procurement costs and shortages.

Another notable concern is the increase in inventory turnover days from 81 to 126 over the past three fiscal years. This trend suggests slower inventory movement, potentially indicating softening demand, accumulating stock, or less efficient inventory management, which could hurt GNG’s liquidity and profitability.

The company aims to repay ₹320 crore in borrowings through the IPO. What will its debt profile look like after this?

GNG’s borrowings increased from ₹113.7 crore in FY23 to ₹434.3 crore in FY25, with a debt-to-equity ratio of 1.92. A repayment of ₹320 crore after the IPO will reduce its debt to nominal levels. The company has met all repayment obligations and covenants so far. While some lender conditions remain, reduced leverage after the IPO is expected to ease financial pressure and increase flexibility.

How scalable is GNG’s business and what factors influence demand for refurbished devices?

The global refurbished electronics market expanded from $60.3 billion in 2018 to $110.6 billion in 2024, registering a compound annual growth rate (CAGR) of 10.7%. It is projected to grow at a 17.4% CAGR between 2024 and 2029 to hit $246.7 billion.

This presents a significant growth opportunity. GNG’s global presence, robust sourcing network, and certified refurbishment capabilities position it to capitalise on this expansion.

However, the industry faces significant hurdles. A lack of uniform standards in the sector leads to inconsistent product quality and performance. Also, ensuring effective and complete data erasure is a persistent challenge, one that poses serious privacy risks that could erode consumer trust in the resale market.

Many consumers are hesitant to buy refurbished products because of their shorter warranties, and the lingering perception that they are subpar. Countering this scepticism and building widespread trust in the reliability and durability of its refurbished products will require a concerted effort.