- The entire IPO is a fresh issue of shares—not a single promoter is selling. That means all the proceeds will go to the company, primarily to support its ongoing projects. Lotus Developers plans to use ₹550 crore of the IPO proceeds for funding construction and development, and the rest for general corporate expenses.

- A long list of marquee names has invested in the company—actors Shah Rukh Khan, Amitabh Bachchan, Tiger Shroff, Manoj Bajpayee, the Roshan family, and seasoned investor Ashish Kacholia. None of them is selling their stake in the IPO, which speaks to their confidence in the company’s future.

- Lotus has priced the offer at ₹140-150 per share, which implies a valuation of ₹7,331 crore at the upper end. This is roughly the same level at which the company raised funds privately from these celebrities in December, despite its profits having doubled since then. That kind of consistency in pricing is rare, especially in a heated IPO market.

What sets Lotus Developers apart from listed peers?

Lotus Developers differentiates itself with its capital-light approach, avoiding the traditional land-acquisition model its peers follow. Instead, the company partners with housing societies and existing property owners through development agreements. This helps minimise upfront capital outlay, enabling the company to earn better returns.

Also, Lotus focuses on greenfield projects and joint development projects. It finances its projects through pre-sales, in line with industry practices. The real differentiator is what it builds and for whom.

What customer segment does Lotus Developers target?

Lotus Developers targets high-net-worth individuals (HNIs) and ultra-HNIs—a fast-growing segment. It focuses on luxury homes priced above ₹3 crore and ultra-luxury offerings above ₹7 crore, catering to a demand category that has gained significant momentum.

Property consultancy Anarock estimates that demand in the ₹2.5 crore-plus segment has grown fourfold, from 3% in 2021 to 12% in the first quarter of 2025-26. This trend is expected to continue as the number of HNIs in the country is projected to double from about 850,000 now to 1.65 million by 2027.

What are Lotus Developers’s key markets?

The company’s projects are concentrated in some of Mumbai’s most premium markets. These include Andheri West, Juhu, Bandra West, and Prabhadevi, where it holds 13% market share in terms of supply and a 12% sales share in units priced above ₹7 crore. Lotus Developers also plans to expand to Mumbai’s Nepean Sea Road and Ghatkopar areas.

Does Lotus Developers enjoy pricing power?

The company commands a premium of around 22% when compared with the average quoted price for similar real estate projects in Juhu. Strong brand recall, high build quality, timely project execution, and customer satisfaction contribute to the premium pricing.

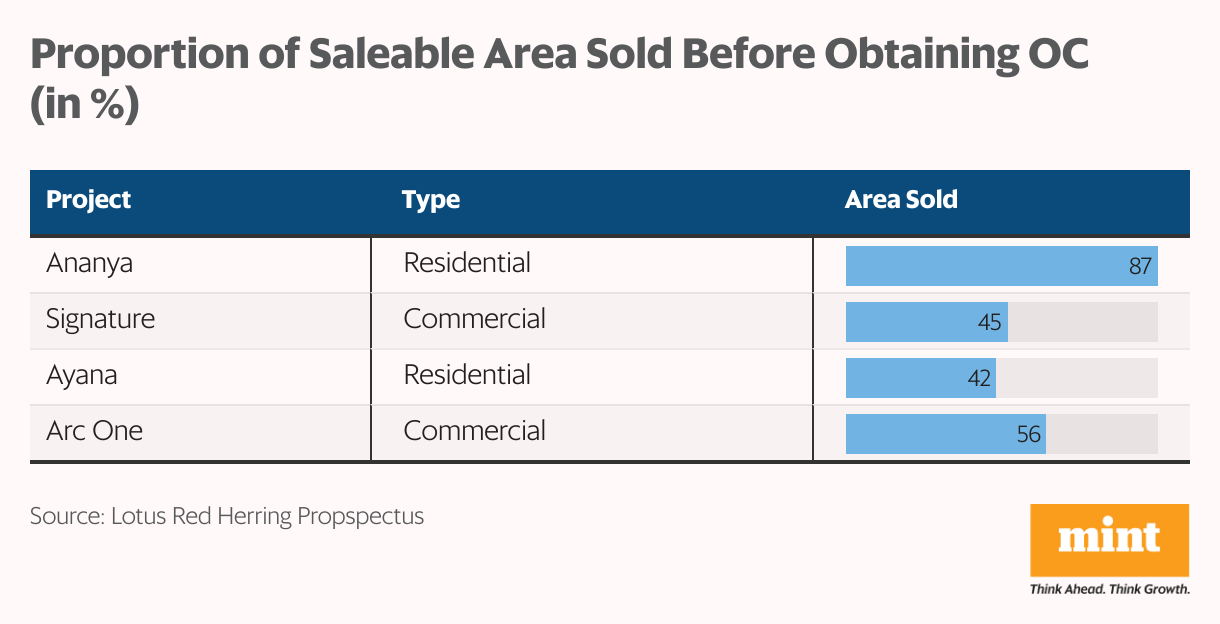

Lotus’s projects also enjoy strong pre-launch demand—more than 50% of the saleable area is typically sold even before occupancy certificates are issued. This reflects both brand confidence and pricing power.

The company also boasts a strong execution track record, completing projects 20 months ahead of schedule, on average. For a sector often plagued by delays, this early-delivery record stands out.

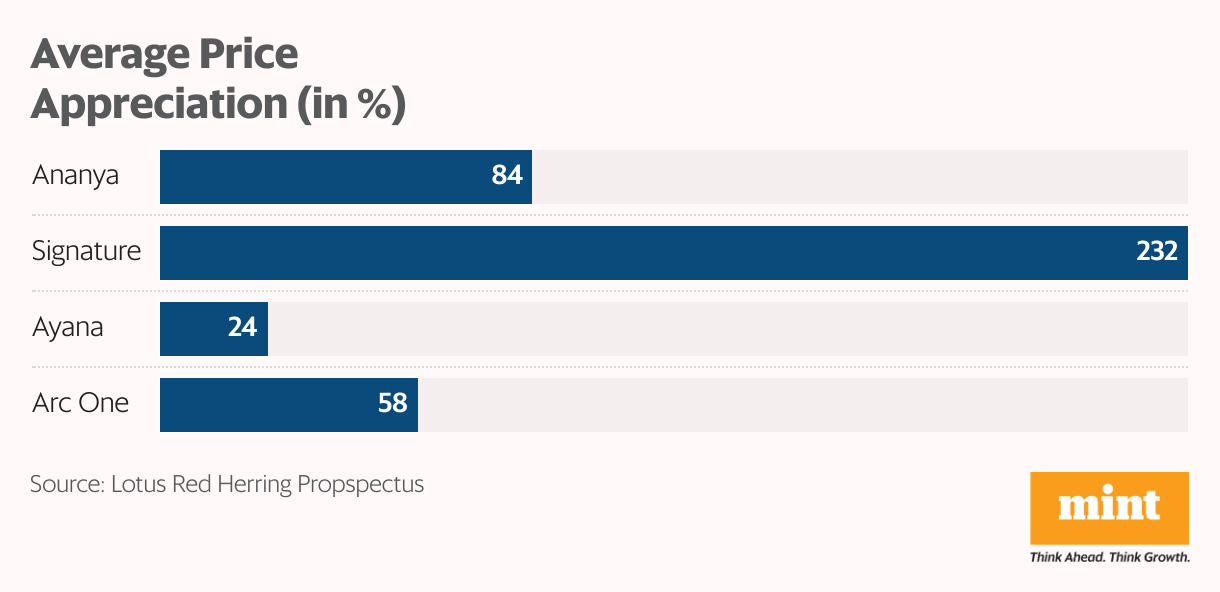

Another differentiator is Lotus Developers’s product customization. Each project is tailored to specific buyer preferences rather than identical units. For instance, its commercial project, Signature, includes private theatres and banquet lounges. Residential projects Ananya and Ayana include rooftop amenities.

This contributes to a strong price appreciation from the time of starting a project to its completion. The Signature project’s price appreciated by 232%, while prices at Ananya and Ayana increased by 24% and 84%, respectively.

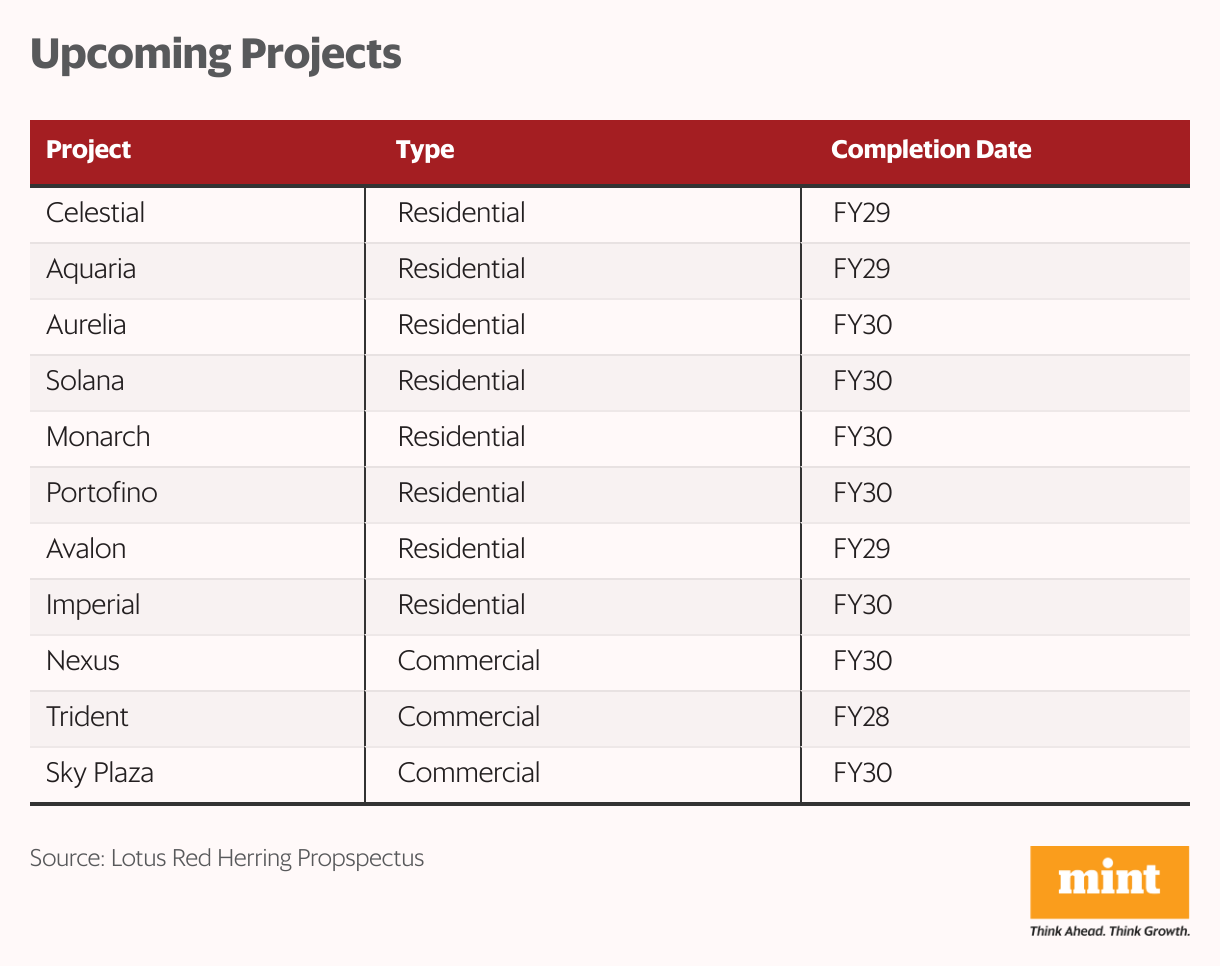

How strong is Lotus’s project pipeline?

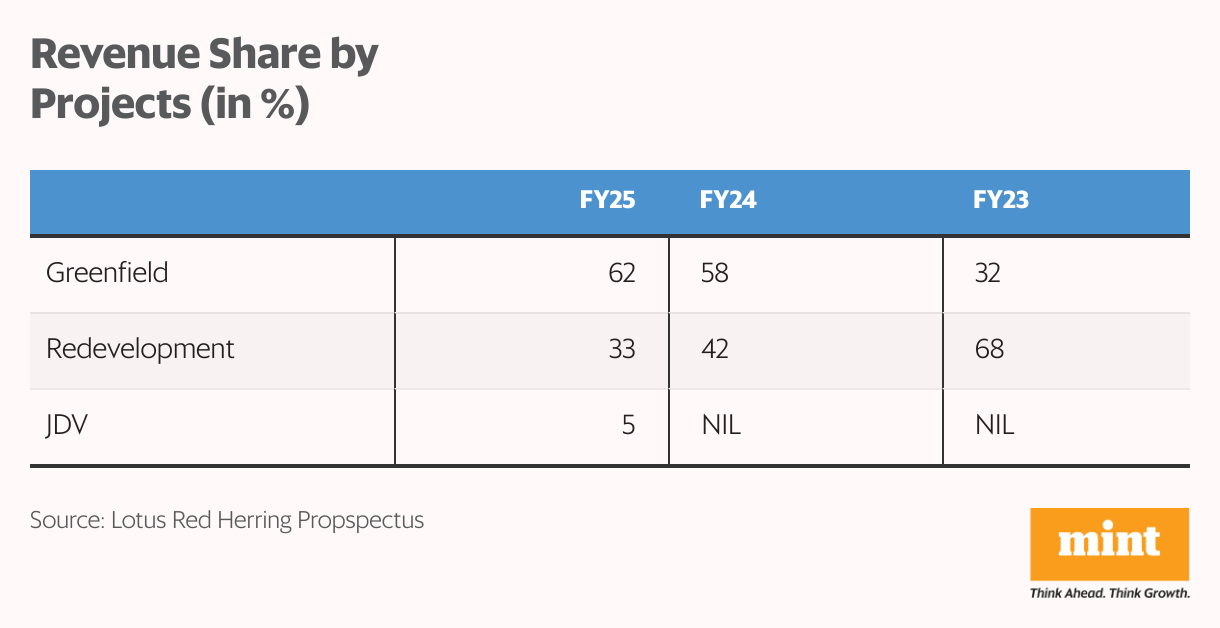

As of June, Lotus had completed four projects comprising 334 units, with a developable area of about 931,448 square feet and saleable area of about 378,396 sq.ft. Redevelopment contributed 54%, while greenfield projects made up the remaining 46%.

Of the 334 completed units, 255 were commercial and 79 were residential. Lotus has not completed any Joint development project yet.

Of the 334 completed units, 255 were commercial and 79 were residential. Lotus has not completed any Joint development project yet.

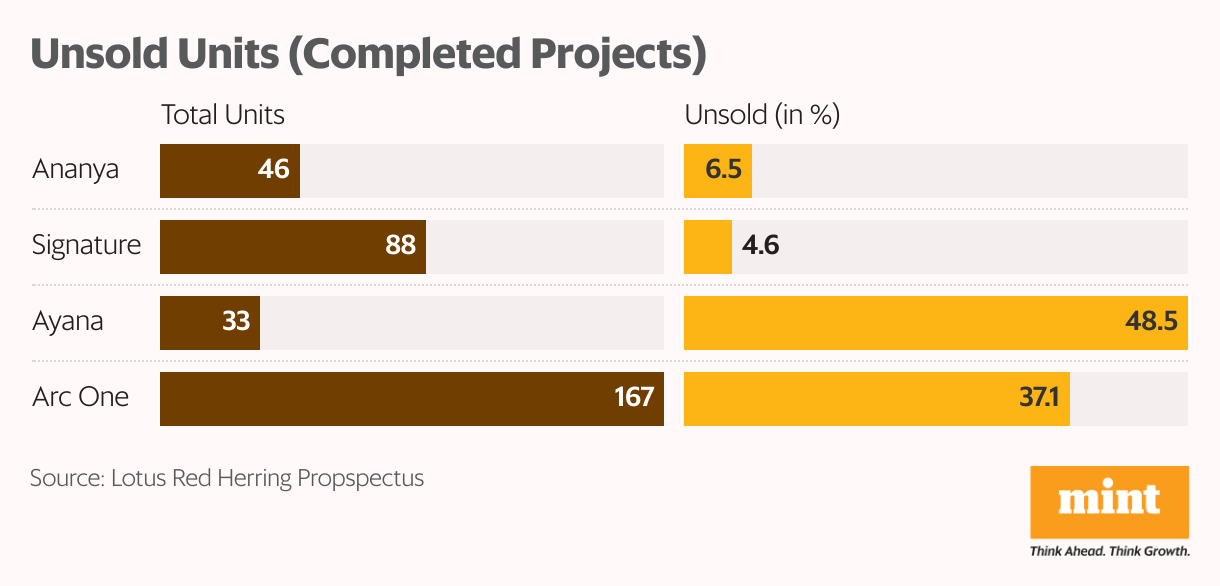

A sizable portion of Lotus’s saleable area and units remains unsold, offering near-term visibility for revenue recognition. Additionally, Lotus has a strong pipeline of ongoing and upcoming projects. The company is now focusing more on residential projects to diversify its revenue mix.

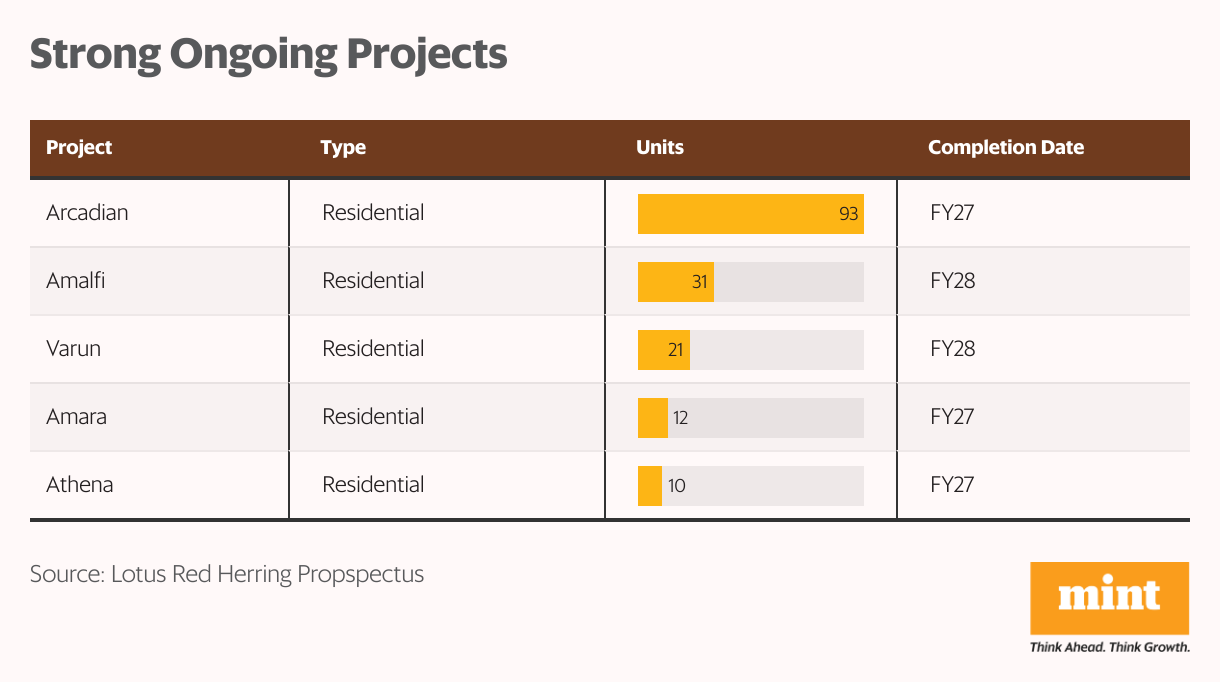

Lotus has five ongoing residential projects comprising 167 units and about 295,586 sq.ft of saleable area. Of this, 115 units are scheduled for completion in FY27, and the rest in FY28. This phased timeline provides steady visibility for revenue recognition over the medium term.

Lotus Developers also has upcoming projects totaling 4.9 million sq.ft. in developable area—over 6x its current developable area—slated for phased completion during FY28-30. If demand in the luxury and ultra-luxury segment holds up, this pipeline could be a strong revenue driver over the medium term.

How is Lotus Developers’s revenue split across segments?

Lotus currently generates revenue from five active projects. While redevelopment accounts for the majority of its developable area, greenfield projects drive most of its topline. The company’s flagship greenfield commercial project, Signature, which received a completion certificate in 2023, accounted for 62% of its revenue in FY25, up from 32% in FY23.

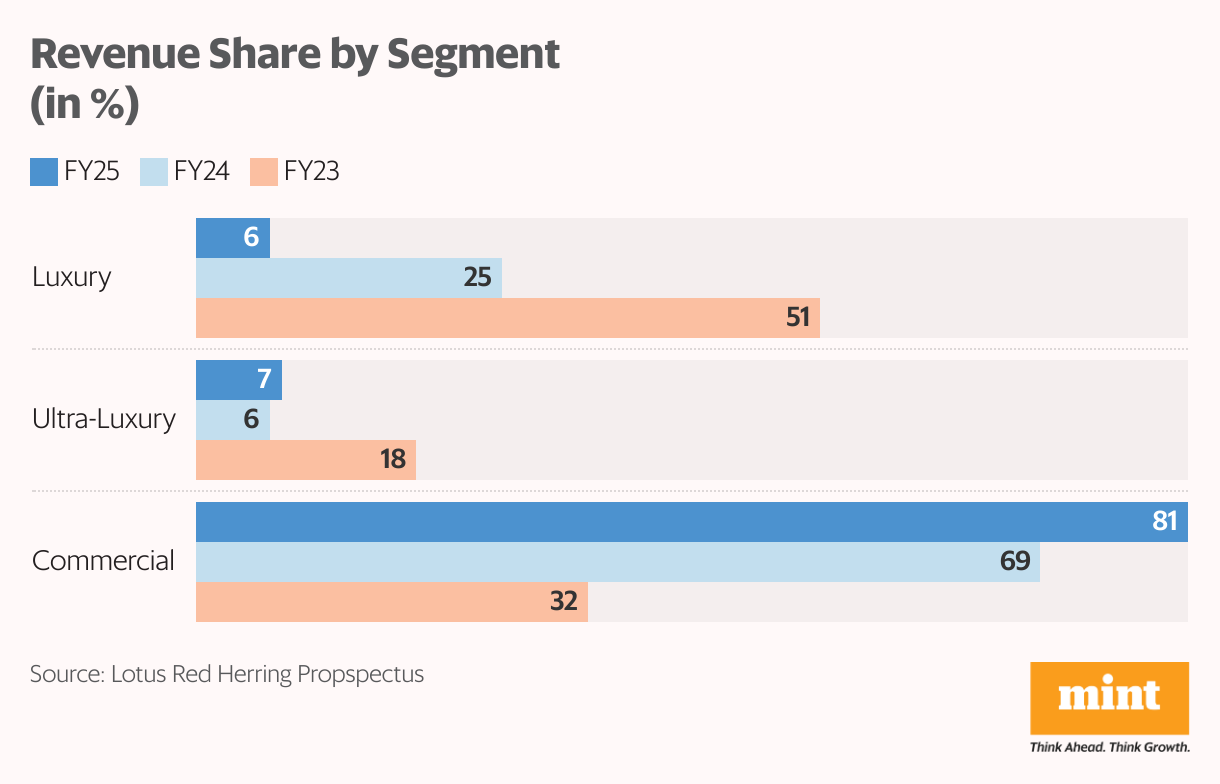

The commercial segment contributed 81% of Lotus’s FY25 revenue of ₹550 crore. Luxury housing made up 6% of FY25 revenue, while ultra-luxury residences contributed 7%—lower than 51% and 18%, respectively, in FY23.

This sharp skew toward commercial revenue has made Lotus’s current revenue concentrated. However, this is expected to diversify in the coming years as more residential projects move toward completion.

How has Lotus performed financially?

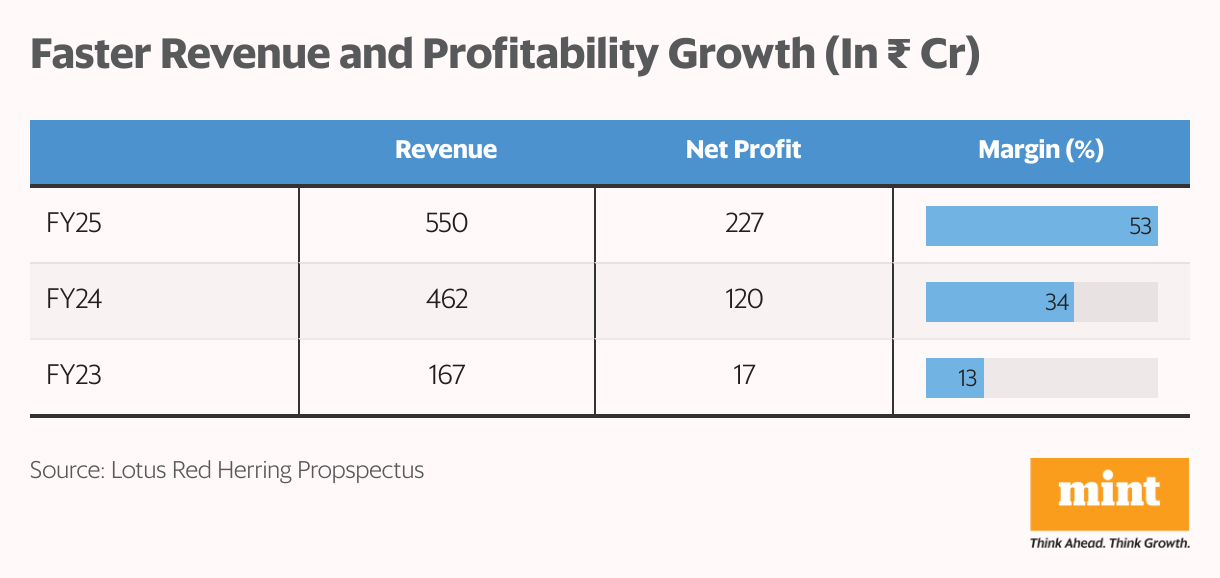

Lotus’s revenue has grown more than threefold in two years, from ₹167 crore in FY23 to ₹550 crore in FY25. Net profit rose faster, jumping 13x to ₹227 crore from ₹17 crore.

The sharp revenue increase has driven a strong operating leverage benefit, with its ebitda margin expanding from 13% in FY23 to 53% in FY25. This is significantly higher than Arkade Developers Ltd’s 30% ebitda margin and Suraj Estate Developers Ltd’s 37%.

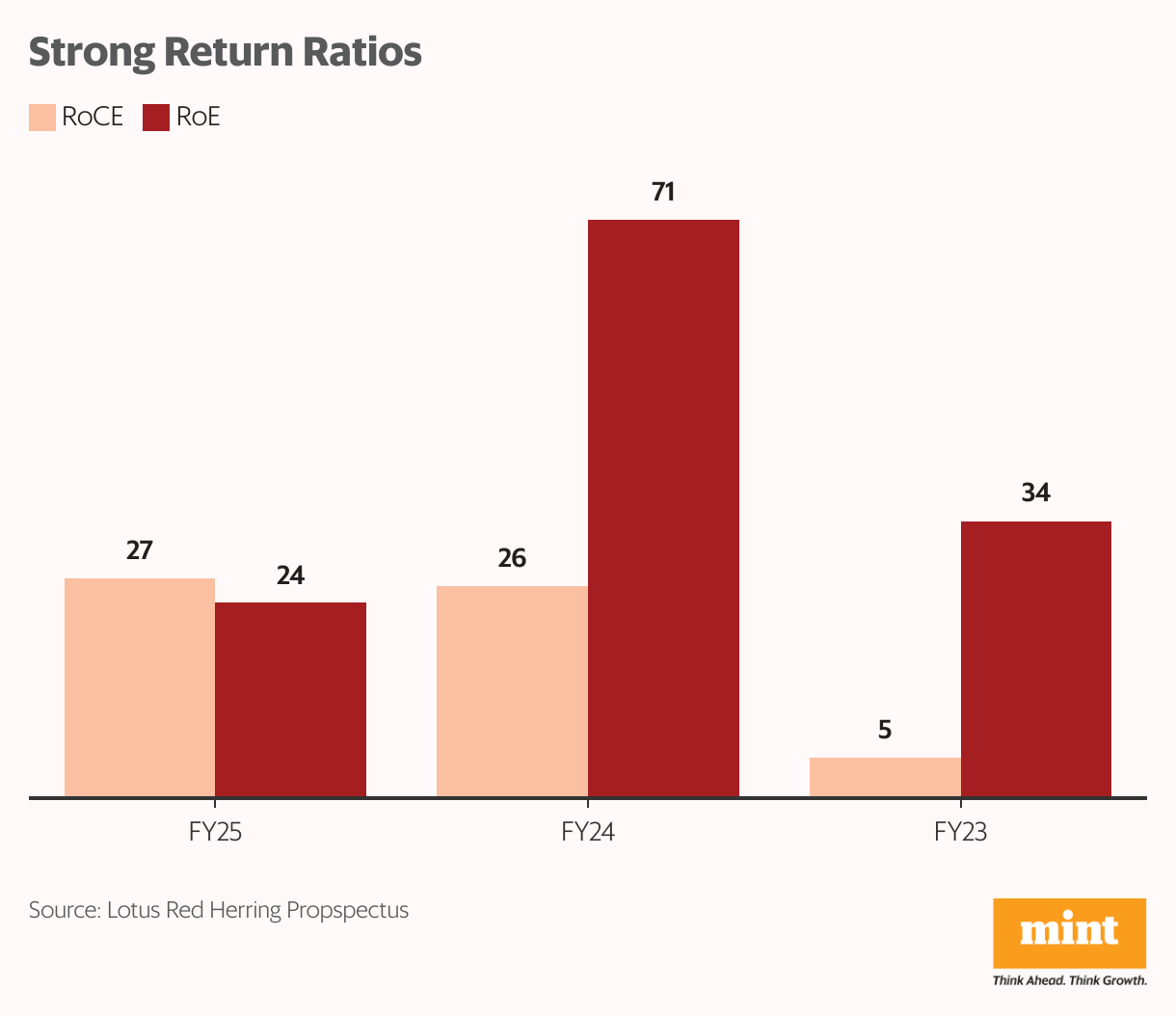

Lotus’s improving margin profile and profitability have translated into strong return ratios. Return on equity (RoE) stands at 24% and return on capital employed (RoCE) at 27%—higher than Arkade’s RoE and RoCE of 18% and 20%, respectively, and Suraj’s 11% and 15%.

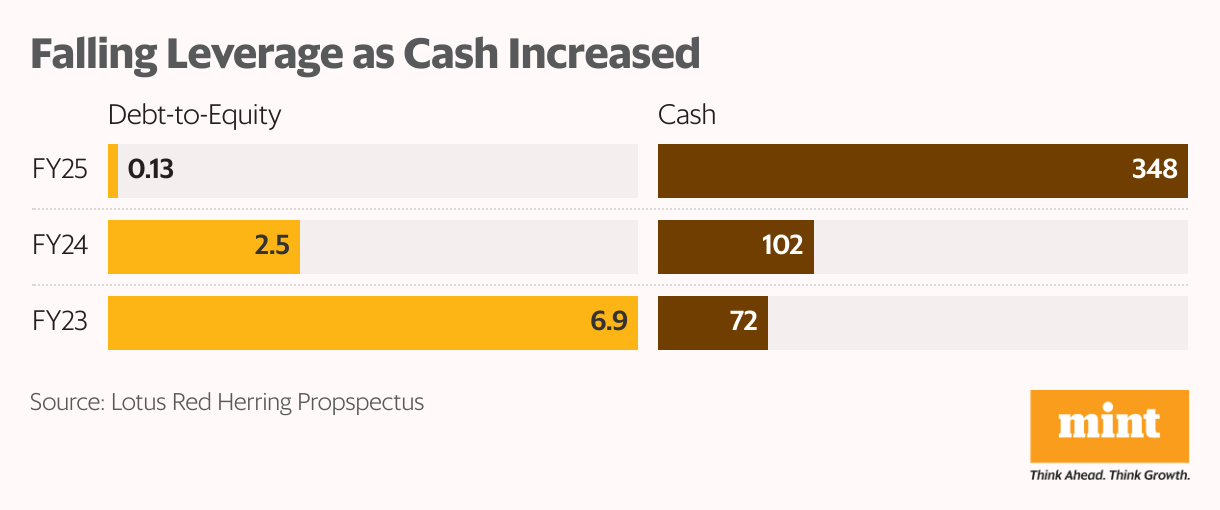

Moreover, as Lotus’s sales ramped up, its cash and cash equivalents grew nearly fivefold, from ₹72 crore in FY23 to ₹348 crore in FY25, helping the company improve its balance sheet significantly. Lotus’s debt-to-equity ratio is now down to 0.13, from a high of 6.9 in FY23.

Lotus’s trade receivables, however, have grown sixfold, from 6% in FY23 to 37% in FY25. Thus, any prolonged delay or inability to recover these receivables could reduce profits and impact cash flows. Higher geographical concentration in Mumbai also poses a risk.

Can Lotus justify its premium and sustain growth?

At a price-to-earnings multiple of 33x, Lotus is asking for a significant valuation premium over peers like Arkade (23x) and Suraj (15x). Even after factoring in a premium for its strong margins, superior return ratios, and industry-leading growth, Lotus’s valuation appears stretched.

The valuation may still be justified provided Lotus sustains its current growth momentum.

That said, residential real estate demand is showing signs of a slowdown. Lotus’s higher exposure to commercial projects, which remains more stable, offers some cushion. The company’s ability to scale up its upcoming projects, which are quite large in size, will be crucial in sustaining growth.

The bigger question is, can Lotus maintain its growth momentum from a larger base?

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.