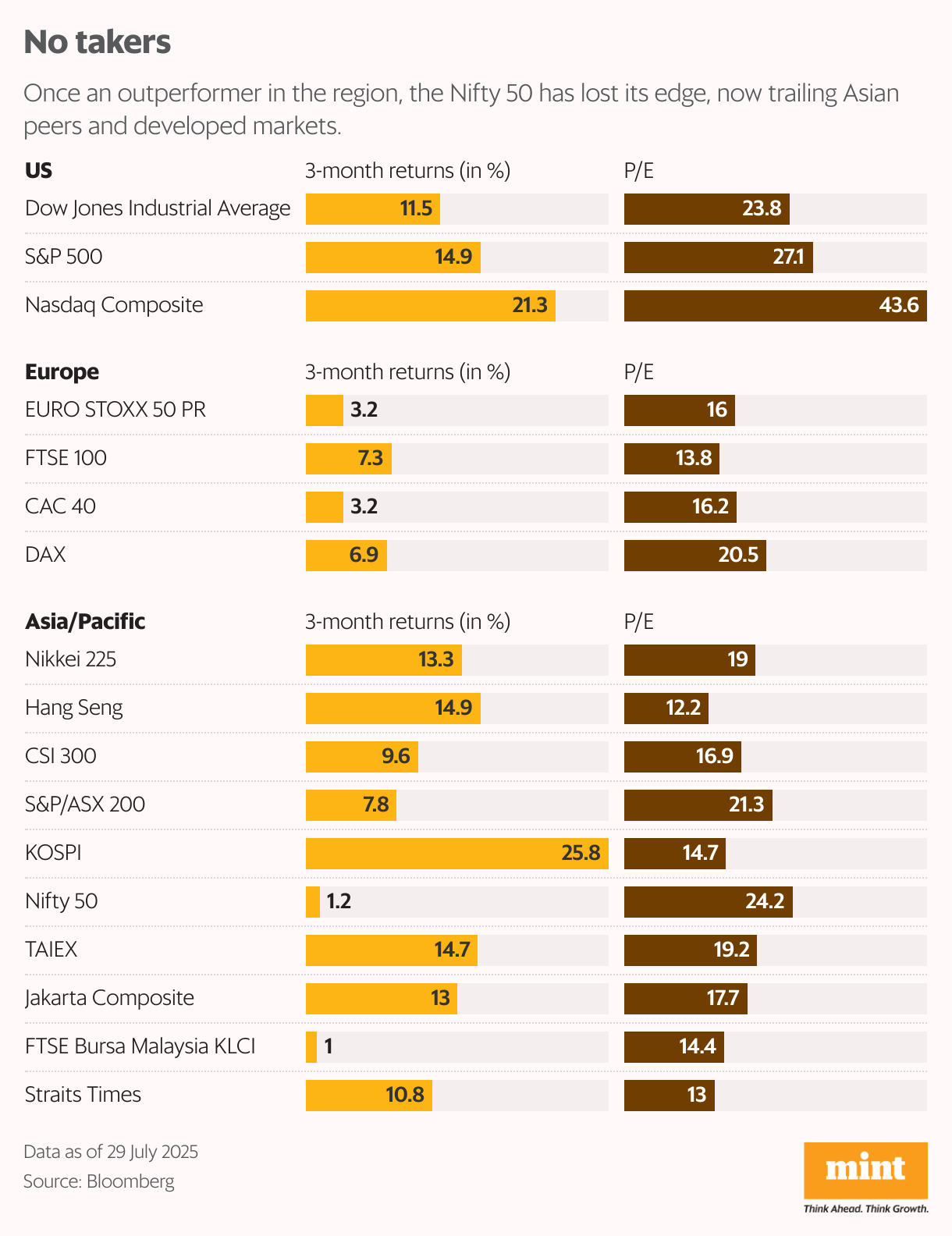

Once regarded as a resilient outperformer in the region, the Nifty 50 has recently lost its edge, slipping into the underperformer bracket and trailing not only its Asian peers, but also several developed markets.

According to Bloomberg data, the Nifty 50 is currently trading at a steep price-to-earnings ratio of 24.2 times, making it one of the priciest markets in Asia. For context, Japan’s Nikkei is at 19x, Taiwan’s Taiex at 19.2x, China’s CSI 300 at 16.9x, South Korea’s Kospi at 14.7x, and Hong Kong’s Hang Seng is way lower at just 12.2x.

Read more: NSDL IPO: Reasonable valuation, strong moat, and room to reclaim growth

Having posted just a 1.2% gain in the past three months, Nifty is barely ahead of Malaysia’s FTSE Bursa Malaysia KLCI, which rose 1%. In fact, Nifty has found itself at the bottom of the Asia pack, while peers like Japan’s Nikkei, Taiwan’s Taiex, and others mentioned above have surged between 8% and 26%, according to Bloomberg data. Even developed markets like the US’ S&P 500 rose 15% in the past three months, while Germany’s DAX is up 7%, the data showed.

“This should have been India’s time to rally especially with the dollar losing strength and emerging market currencies gaining ground. But instead, the economic slowdown and expensive stock valuations are keeping foreign investors at bay,” said Saurabh Mukherjea, founder and chief investment officer (CIO) at Marcellus Investment Managers.

Beyond the weariness from persistent valuation concerns, a major factor behind the underperformance of Indian equities relative to other markets has been the lingering global economic uncertainty, said Nirav Karkera, head of research at Fisdom.

“There’s growing uncertainty around the US economic direction and its monetary policy stance. At the same time, trade protectionism is quietly picking up across the globe, partly as a ripple effect of the US tariff actions. This mix is making global investors nervous,” he added.

Even with steady domestic inflows through systematic investment plans (SIPs), the Indian mutual fund industry continues to hold a sizeable cash pile, reflecting a cautious stance. At the same time, foreign investor confidence remains patchy, with their buying activity still lacking consistency.

Since January, domestic institutional investors (DIIs) have consistently pumped money into equities every single month, with net purchases totaling a massive ₹4.04 trillion, according to BSE data. Foreign institutional investors (FIIs), on the other hand, have been far less predictable. After starting the year as net sellers, FIIs briefly turned buyers from March to June, only to return to the selling mode in July. Overall, FIIs have pulled out ₹1.28 trillion from Indian equities so far this year, as per NSDL data.

Read more: Bulls and bears clash at 25,200: Will Nifty break free?

Besides, market experts say this hesitation stems from subdued consumption trends, and a slower-than-expected earnings recovery – all of which are weighing on market sentiment and keeping capital at bay.

Other weak spots

The ongoing impasse in trade talks between the US and India remains a significant worry for investors, with no clear resolution in sight. This uncertainty adds to the overall discomfort in the market.

The two sides remain in discussions over an interim trade agreement, as the 1 August deadline approaches. The date marks the end of the suspension period for tariffs—up to 26%—originally imposed by US President Donald Trump on several countries, including India. According to reports, a US delegation is scheduled to visit India on 25 August for the next round of talks on the trade deal.

On the corporate front, while Q1 FY26 financial results have been a mixed bag, Karkera noted that the recovery in India Inc’s earnings may be delayed by up to two quarters. “Even the earnings of index heavyweights have struggled to captivate investors, which signals that the anticipated earnings growth might take longer to materialize than originally expected,” he explained.

The Nifty 50 has recorded single-digit profit growth for the last seven quarters, except in Q1 FY25, when it saw a de-growth of nearly 7%, Bloomberg data shows. For Q1 FY26, so far 25 companies in the index have reported their earnings, with an average profit growth of about 5% year-on-year.

What would revive the momentum?

“Our economy has entered a cyclical downturn and the earnings growth has slowed over the last four quarters… it’s not evident whether it will revive any time soon,” said Mukherjea of Marcellus Investment Managers.

Vinay Jaising, CIO and head of equity advisory at ASK Private Wealth, which manages over ₹44,000 crore in assets, highlighted a notable trend: while Indian equities have underperformed compared with the global markets, capital is still flowing into riskier assets such as US equities.

He said even though the blue-chip or large-cap indices have remained flat over the past three months, the Nifty Smallcap 250 has gained nearly 11%, indicating that select investors are still chasing growth and higher-risk opportunities.

Read more: Kotak Bank trades at a discount to top private peers. A key ratio reveals why

“What could potentially drive a sustained upward momentum in headline Indian equities is a recovery in earnings growth, especially in B2C (Consumption), which still appears to be one or two quarters away, and a revival in private capex, which is yet to reflect the benefits of recent interest rate cuts,” Jaising added.

Indian companies have been slow to ramp up capital expenditure, despite the Reserve Bank of India cutting policy rates by total 100 basis points since February, its first easing move in five years. The muted response reflects lingering caution.

For the Indian markets to inch higher, “we must maintain the earnings growth momentum,” said Alok Singh, CIO at Bank of India MF.

“While there are concerns, such as muted revenue growth and lacklustre private capex, these do not warrant an immediate de-rating,” Singh said. However, if these issues persist, a “gradual de-rating” in valuations is likely over time, he added.

The outlook for equity returns largely depends on a revival in consumption and a rebound in earnings growth, factors that could also help restore foreign investor confidence in Indian markets.

Read more: FPIs struggle to shake off fears, bearish bets hit 4-month high